Disclaimer: The information on this website is for general educational purposes only and does not constitute financial advice. The content does not take into account your personal objectives, financial situation, or needs. Superannuation, tax, and investment laws are complex and subject to change. All readers are strongly encouraged to conduct their own research and seek professional advice from a licensed financial advisor or registered tax agent before making any financial decisions.

For millions of Australians, June 1, 2023, delivered a profound financial shock. On that day, an indexation rate of 7.1% was applied to their Higher Education Loan Program (HELP) debts, a figure unseen in decades. This single event transformed what was long considered a benign, low-cost "good debt" into a significant source of anxiety and a pressing financial question. The average HECS-HELP debt, which stood at $26,494 in 2022-23, suddenly felt much heavier.

So, what's the right move now? This has ignited a fierce debate, pitting decades of conventional financial wisdom against a new economic reality. The long-held advice was simple: make your compulsory repayments and otherwise ignore your HECS debt, directing spare cash towards higher-return investments. But with indexation rates rivalling mortgage interest rates, is that advice still sound? Are individuals better off aggressively paying down their student loans, or is that a decision that carries a significant, and potentially costly, opportunity cost?

Key Takeaways: HECS Repayment in 2025

- Reforms De-Risk HECS: The 2025 government reforms (WPI indexation cap, a 20% debt cut, and lower repayment thresholds) have made holding HECS debt much safer and cheaper.

- Home Loans are the Exception: The biggest practical reason to pay HECS early is to increase your mortgage borrowing capacity. For many, this is the deciding factor.

- Investing Often Wins: For long-term wealth creation, investing surplus cash in assets like ETFs or superannuation will likely outperform the money saved by paying off low-cost HECS debt.

- It's a Personal Decision: The right choice depends on your personal goals, risk tolerance, and especially your timeline for buying a home.

Section 1: Decoding Your HECS-HELP Debt: The Complete Picture

Before you can decide whether to pay it off or invest, you first need to know exactly how HECS-HELP debt works. To make an informed decision, a foundational understanding of the HECS-HELP system is essential. The mechanics of how the debt is accrued, repaid, and indexed contain nuances that are critical to the strategic choices that follow.

HECS-HELP Fundamentals

Australia's Higher Education Loan Program (HELP) is the overarching government scheme providing loans to students for their tuition fees. The most common type of loan within this program is HECS-HELP, which is available to eligible students enrolled in a Commonwealth Supported Place (CSP) at a university or approved higher education provider. In a CSP, the government subsidises a portion of the course cost, and the student is responsible for the remainder, known as the "student contribution amount," which can be deferred via a HECS-HELP loan.

The core design of the scheme is an income-contingent loan, not a conventional commercial loan. It is technically interest-free, with repayments managed through the Australian Taxation Office (ATO). There is a lifetime borrowing limit, known as the 'available HELP balance'. For 2025, this limit is $121,844 for most students, and higher for specific courses like medicine. Any repayments made to the ATO re-credit this balance, allowing for further study if needed.

The Mechanics of Repayment

Repayments for HECS-HELP debt fall into two distinct categories: compulsory and voluntary.

Compulsory Repayments

These repayments are automatically triggered once an individual's 'Repayment Income' (RI) for a financial year exceeds a government-set threshold. For the 2024–25 income year, this threshold is $54,435. When an employee with a HECS-HELP debt starts a job, they notify their employer, who then withholds an additional amount from their regular pay under the Pay As You Go (PAYG) system to cover the anticipated compulsory repayment. The ATO calculates the exact repayment amount when the individual lodges their annual tax return.

A crucial point of clarification is the definition of Repayment Income (RI). It is broader than just taxable salary and is calculated as an individual's taxable income plus any total net investment losses (including rental losses), reportable fringe benefits, reportable superannuation contributions, and exempt foreign employment income.

Voluntary Repayments

An individual can choose to make extra payments directly to the ATO at any time to reduce their loan balance. These are known as voluntary repayments. It is critical to understand that voluntary repayments are made in addition to any compulsory repayment obligations for that year; they do not offset or reduce the compulsory amount calculated on a tax return. Furthermore, these payments are non-refundable.

The Engine of Growth: How Indexation Really Works

While the loan is "interest-free," the outstanding balance does not remain static. To maintain its real value over time, the debt is indexed annually on June 1st. This indexation is only applied to the portion of the debt that is 11 months or older.

The New Calculation Method

Historically, the indexation rate was tied to the Consumer Price Index (CPI), a measure of inflation. However, the 7.1% CPI-linked rate in 2023 caused public outcry as it significantly outpaced wage growth. In response, the government passed legislation that fundamentally changed the calculation. The indexation rate is now capped at the lower of either the CPI or the Wage Price Index (WPI). This change, backdated to June 1, 2023, ensures that HECS-HELP debt can no longer grow faster than average wages, a critical de-risking of the loan for all holders.

Historical Context

The significance of this change is best understood by looking at the historical rates. For a decade prior to 2022, indexation was a non-issue, hovering in a low and stable range. The 2023 spike was an anomaly that triggered a permanent policy shift.

Historical HECS Indexation Rates

| Year (as at June 1) | Original Rate (CPI) | Final Rate (Lower of CPI/WPI) |

|---|---|---|

| 2014 | 2.6% | 2.6% |

| 2015 | 2.1% | 2.1% |

| 2016 | 1.5% | 1.5% |

| 2017 | 1.5% | 1.5% |

| 2018 | 1.9% | 1.9% |

| 2019 | 1.8% | 1.8% |

| 2020 | 1.8% | 1.8% |

| 2021 | 0.6% | 0.6% |

| 2022 | 3.9% | 3.9% |

| 2023 | 7.1% | 3.2% |

| 2024 | 4.7% | 4.0% |

| 2025 | 3.2% | 3.2% |

Source: Australian Taxation Office

The Timing Mismatch That Fuels Debt Growth

Ever felt like your HECS balance keeps growing even though you're making repayments? You're not imagining it. A common source of frustration for HECS-HELP debtors is the feeling that their balance continues to grow despite making regular repayments. This is not an illusion; it is a direct result of a structural timing mismatch in the ATO's collection and application process.

The process unfolds as follows:

- Throughout the financial year (July 1 to June 30), an employer withholds extra tax from an employee's pay to cover their compulsory HECS-HELP repayment.

- Many assume this money is progressively applied to their loan balance. This is incorrect. The ATO holds these withheld amounts as a tax credit and does not apply them to the HECS-HELP account until the individual lodges their tax return, which can only happen after June 30.

- However, indexation is calculated on the entire outstanding loan balance as it stands on June 1st of that year.

- This means that a full year's worth of compulsory repayments sits with the ATO, unapplied, while indexation is calculated on a principal amount that is artificially high.

This timing issue is a primary driver of the sentiment that the debt is "running away" and provides the single most compelling tactical argument for making a voluntary repayment. By making a voluntary payment before the June 1st deadline, an individual can directly reduce the principal amount that will be subject to indexation, thereby saving money.

Section 2: A New Playing Field: How 2025 Government Reforms Change Everything

The financial calculus of holding HECS-HELP debt has been fundamentally altered by a suite of government reforms that have now passed into law. These changes provide significant relief to debtors and have de-risked the loan for the long term.

The Backdated Relief: Indexation Credits for 2023 & 2024

As a direct result of the new WPI cap, the unusually high indexation rates from the past two years were retrospectively lowered:

- The rate for 1 June 2023 was reduced from a staggering 7.1% down to 3.2%.

- The rate for 1 June 2024 was reduced from 4.7% down to 4.0%.

The ATO automatically applied these changes as an "indexation credit" to the accounts of all affected individuals, effectively reducing their outstanding debt. This single measure wiped approximately $3 billion from the nation's collective student loan balance.

The One-Off Windfall: The 20% Debt Reduction

In a landmark move, the government has legislated a one-off 20% reduction for all outstanding HELP and other eligible student loan balances that existed as at 1 June 2025. This measure, part of the government's response to the Australian Universities Accord, is designed to provide broad cost-of-living relief and will benefit over 3 million Australians.

The mechanics of this reduction are crucial: the 20% cut is applied to an individual's loan balance before the 2025 indexation is calculated. The ATO will then apply the 2025 indexation rate (3.2%) to the new, lower balance. For a person with the average debt of $26,500, this represents a direct reduction of $5,300. Nationally, this policy is expected to remove over $16 billion in student debt.

A Fairer System? The New Marginal Repayment Thresholds

The third major reform, effective from the 2025–26 income year, is a complete overhaul of the compulsory repayment system. Previously, the repayment rate was applied to a person's entire Repayment Income (RI). The new system is marginal, meaning repayments are only calculated on the portion of income above the minimum threshold.

The new thresholds and rates are as follows:

- The minimum repayment threshold has been significantly increased to $67,000.

- For income between $67,001 and $125,000, the repayment is 15 cents for each dollar earned above $67,000.

- For income above $125,001, the repayment is $8,700 plus 17 cents for each dollar earned above $125,000.

- A cap remains where those earning $179,286 or more will repay 10% of their total RI to ensure they are not worse off under the new system.

The practical effect of this change is a lower compulsory repayment for most individuals. For example, consider a person named Grace with a Repayment Income of $80,000:

- Under the old system (2024–25 rates): Her repayment rate would be 3.5%. The repayment would be calculated on her entire income: $80,000 * 3.5% = $2,800.

- Under the new system (2025–26 rates): She only pays on the income above the threshold: ($80,000 - $67,000) * 15% = $13,000 * 15% = $1,950.

This change reduces her annual compulsory repayment by $850, increasing her take-home pay.

Compulsory Repayment: Old vs. New System

| Repayment Income (RI) | 2024-25 Compulsory Repayment ($) | 2025-26 Compulsory Repayment ($) | Annual Reduction ($) |

|---|---|---|---|

| $65,000 | $1,300 (2.0%) | $0 | $1,300 |

| $80,000 | $2,800 (3.5%) | $1,950 (15% on income > $67k) | $850 |

| $100,000 | $5,500 (5.5%) | $4,950 (15% on income > $67k) | $550 |

| $120,000 | $8,400 (7.0%) | $7,950 (15% on income > $67k) | $450 |

Sources: ATO, Budget 2024-25

These three reforms—capping the indexation rate, reducing the principal, and lowering the minimum repayments—represent a systematic de-risking of HECS-HELP debt by the government. The primary financial risk that emerged in 2023, where indexation could outpace wage growth and erode an individual's financial position, has been directly addressed and mitigated through policy. This makes the purely mathematical case against making voluntary repayments significantly stronger than it was prior to these changes.

Section 3: Is HECS "Good Debt" or "Bad Debt"? A Financial Framework

So, where does HECS actually fit in? Is it a "good debt" like a mortgage or a "bad debt" like a credit card? To properly analyse the decision of early repayment, it is useful to frame it within the well-established personal finance concept of "good debt" versus "bad debt".

Defining the Spectrum of Debt

In personal finance, debt is not viewed monolithically; it exists on a spectrum of utility.

- Good Debt: This is typically defined as borrowing for the purpose of acquiring an asset that is expected to increase in value or generate income over time. The loan is an investment in one's future net worth. Classic examples include a mortgage to buy a home, a loan to start or expand a business, or a loan to purchase an investment property or shares.

- Bad Debt: This refers to borrowing for consumption or to purchase assets that depreciate rapidly in value. It is often characterised by high interest rates and provides no long-term financial benefit. As ASIC's MoneySmart explains, common examples include high-interest credit card balances carried from month to month, personal loans for holidays, and some car loans.

The Case for HECS as "Good Debt"

By traditional definitions, HECS-HELP debt fits squarely in the "good debt" category. It is an investment in one's "human capital"—the skills, knowledge, and qualifications that enhance future earning capacity. The premise is that a tertiary education will lead to higher lifetime earnings, providing a positive return on the investment made via the loan.

Furthermore, the loan possesses highly favourable terms that distinguish it from commercial debt. There is no commercial interest rate, repayments are contingent on income (providing a safety net during periods of unemployment or low earnings), and the debt is cancelled upon death.

The Counterargument: When "Good Debt" Feels Bad

Despite its favourable structure, HECS-HELP debt often carries a negative psychological weight. For many individuals, any form of debt is a source of stress, and watching the balance increase each year due to indexation can be demoralising, irrespective of the underlying financial logic.

More tangibly, HECS-HELP debt has a direct and often significant impact on an individual's ability to secure a home loan. As it reduces disposable income in the eyes of a lender, it acts as a practical barrier to achieving a major life goal. This practical drag can make the debt feel like bad debt, even if it does not fit the technical definition.

HECS as a Unique Hybrid Debt

Ultimately, the binary classification of "good" or "bad" is an oversimplification for HECS-HELP. It is more accurately described as a unique hybrid financial instrument. While it shares the investment characteristics of good debt, it is tied to an intangible asset (human capital) rather than a tangible one like property. It has repayment terms far more flexible than any bad debt, yet its very existence can hinder other financial goals. Crucially, its terms are not fixed by a contract but are subject to government policy, which can be altered retrospectively, as the 2025 reforms demonstrate. Understanding HECS-HELP as a unique government-facilitated investment in oneself, with terms unlike any commercial product, is key to appreciating the complexity of the repayment decision.

Section 4: The Case for Early Repayment: Arguments for Clearing Your Debt

While the mathematical case for keeping HECS debt is often strong, there are several compelling strategic, practical, and psychological reasons why an individual might choose to make voluntary repayments.

Argument 1: Avoiding Indexation Compounding

Although the indexation rate is now capped to prevent it from growing faster than wages, it is not zero. In a typical economic environment, it is likely to be between 2% and 4% per year. By making voluntary repayments, especially before the June 1st deadline, an individual reduces the principal balance on which this future indexation is calculated. Over the life of a large loan, this can result in significant savings. For those with substantial debts (e.g., over $50,000 from postgraduate or multiple degrees), even a modest indexation rate translates into a considerable dollar increase each year, making the case for reducing the principal more attractive.

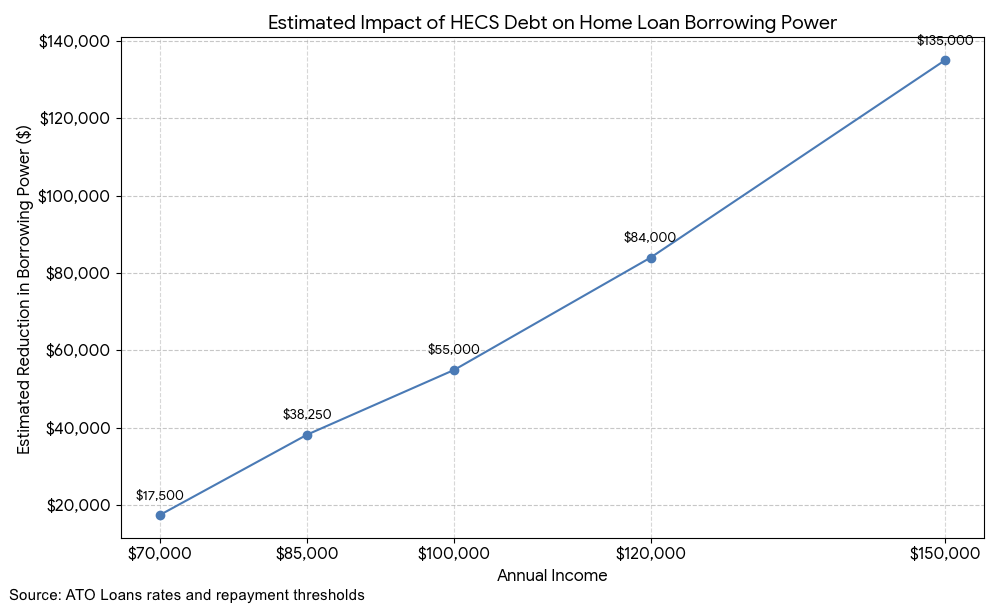

Argument 2: Unlocking Your Borrowing Power for a Home Loan

So, if you're asking yourself, 'is it really worth paying off my HECS early to buy a house?', for many, the answer is yes. This is arguably the most powerful practical reason to pay off HECS-HELP debt early. When assessing a mortgage application, lenders perform a serviceability calculation to determine an applicant's ability to repay the loan from their disposable income. Compulsory HECS-HELP repayments are treated as a non-discretionary expense, directly reducing this calculated disposable income and, therefore, the maximum amount the bank is willing to lend.

As the chart clearly illustrates, the impact of this is often disproportionately large. A common rule of thumb used by mortgage brokers is that an individual's borrowing power can be reduced by approximately 10 times the value of their annual HECS repayment. The table below breaks down these numbers, showing how even a modest income can lead to a significant reduction in borrowing capacity.

Estimated Impact on Borrowing Power (2024-25 Rates)

| Annual Income | HECS Repayment Rate | Annual Repayment ($) | Estimated Reduction in Borrowing Power ($) |

|---|---|---|---|

| $70,000 | 2.5% | $1,750 | ~$17,500 |

| $85,000 | 4.5% | $3,825 | ~$38,250 |

| $100,000 | 5.5% | $5,500 | ~$55,000 |

| $120,000 | 7.0% | $8,400 | ~$84,000 |

| $150,000 | 9.0% | $13,500 | ~$135,000 |

Sources: ATO, standard mortgage broker estimations.

Recognising this barrier, some major banks have begun to introduce more nuanced policies:

- Commonwealth Bank (CBA): As of April 2025, CBA will completely disregard a HECS-HELP debt in its serviceability assessment if the borrower is on track to pay it off within 12 months. Furthermore, for those who will clear their debt within five years, CBA will reduce the mandatory serviceability buffer (the stress-test interest rate) from 3% to just 1%. This can increase borrowing capacity by over $100,000 for some applicants.

- National Australia Bank (NAB): From July 2025, NAB will disregard any HECS-HELP debt with an outstanding balance of $20,000 or less.

These policy shifts create specific, high-value scenarios where a targeted voluntary repayment to get a balance below a certain threshold or within a specific repayment timeframe can unlock a significantly larger mortgage.

Disclaimer: These policies are subject to change and are provided as examples of how lenders are adapting. You should always confirm the current policies directly with any lender as part of your own research.

Argument 3: The Psychological Payoff of Being Debt-Free

Personal finance is as much about behaviour and emotion as it is about spreadsheets. For many people, the knowledge that they owe money, even a low-cost debt like HECS, is a source of persistent mental stress. The peace of mind and sense of financial freedom that comes from being completely debt-free is a valid and powerful motivator. For these individuals, the psychological benefit of eliminating the debt can outweigh the purely mathematical opportunity cost of not investing the funds elsewhere.

Argument 4: Freeing Up Future Cash Flow

Clearing a HECS-HELP debt results in an immediate and permanent increase in an individual's take-home pay, as the compulsory repayments cease. This can be particularly valuable for those planning for a period of reduced or uncertain income, such as starting a business, taking extended parental leave, or moving overseas. Having a higher, more predictable cash flow can provide crucial financial flexibility during these life stages.

Section 5: The Case for Keeping Your HECS: The Power of Opportunity Cost

The arguments against making voluntary repayments are grounded in financial optimisation, focusing on the unique, borrower-friendly nature of the loan and the superior returns potentially available elsewhere.

Argument 1: It's (Almost Always) Your Cheapest Debt

A fundamental principle of debt management is to create a repayment hierarchy based on interest rates. High-interest, non-deductible debts should always be the priority. This includes:

- Credit card debt (often accruing interest at ~20% p.a.)

- Personal loans and car loans (often 7-12% p.a.)

- Even a standard variable rate mortgage (often 6%+ p.a.)

With HECS-HELP indexation now capped and likely to average 2-4% in a normal economic cycle, it is financially the "cheapest" debt most people will ever have. From a purely mathematical standpoint, every available dollar should be directed at higher-cost debts before a single voluntary repayment is made to HECS-HELP.

Argument 2: The Investor's Gambit – Opportunity Cost

But what could your money be doing instead? This is the central mathematical argument against early repayment. Every dollar used to make a voluntary HECS-HELP repayment is a dollar that cannot be invested. This is known as the opportunity cost. If those funds can be invested in an asset that generates a long-term return higher than the HECS indexation rate, the investor will be in a better financial position over time.

Potential investment avenues that have historically outperformed HECS indexation include:

- Australian Shares (ETFs): The Australian share market, as measured by broad market indices like the S&P/ASX 200, has historically delivered long-term total returns in the range of 7-10% per annum.

- Superannuation: This is a highly tax-efficient investment vehicle. Concessional contributions are typically taxed at a flat rate of 15%, which is significantly lower than the marginal tax rate for most income earners. This immediate tax benefit, combined with long-term compound growth within the fund, makes it a powerful wealth-building tool.

- Mortgage Offset Account: For homeowners, placing surplus funds into an offset account linked to their variable-rate mortgage provides a guaranteed, risk-free, and tax-free "return" equal to their home loan interest rate. With mortgage rates often above 6%, this is a highly effective strategy that comfortably beats the HECS indexation rate.

Argument 3: The First Home Buyer's Dilemma – Deposit vs. Debt

While HECS-HELP debt reduces borrowing capacity, the primary obstacle for most first-home buyers is accumulating a sufficient deposit. Using spare cash to make voluntary HECS repayments directly depletes the funds available for a deposit. In many cases, it is more advantageous to have a larger deposit—which can help avoid the significant cost of Lenders Mortgage Insurance (LMI) and secure a better interest rate—than it is to have a marginally higher borrowing capacity due to a lower HECS balance.

Argument 4: The Unique Safety Nets of HECS

The HECS-HELP loan comes with unique features that no commercial loan offers, making it less risky to hold.

- Income-Contingent Repayments: If an individual's income falls below the repayment threshold due to job loss, illness, or career change, the compulsory repayments automatically pause. This provides a crucial safety net that prevents financial hardship.

- Cancellation Upon Death: Unlike nearly all other forms of debt, any outstanding HECS-HELP balance is cancelled upon the debtor's death. It is not passed on to their family or claimed from their estate (with the exception of any compulsory repayment due for their final tax return). This means that money used to pay off the debt is permanently gone, whereas money placed in an investment would form part of the estate available to beneficiaries.

Section 6: Let's Run the Numbers: HECS Repayment vs. Investing

To quantify the opportunity cost, this section models the financial outcome of a common scenario: an individual with a spare lump sum deciding between paying down their HECS-HELP debt and investing it over a 10-year period.

Scenario Setup

- Protagonist: Alex, who has the Australian average HECS-HELP debt of $26,500.

- The Decision: Alex has received a $10,000 lump sum.

- The Two Paths:

- Path 1: Make a $10,000 voluntary repayment to the ATO.

- Path 2: Invest the $10,000.

- Key Assumptions:

- Time Horizon: 10 years.

- Average annual HECS Indexation Rate: 3.0%.

- Alex's Income: $90,000 p.a. (constant for simplicity), resulting in a compulsory HECS repayment of $4,050 p.a. under 2024-25 rates (4.5%).

- Alex's Marginal Tax Rate: 32.5% (+ 2% Medicare Levy) = 34.5%.

- Investment returns are total returns (capital growth plus distributions).

Investment Scenarios Modelled

Three common investment options are considered for Path 2:

- High-Interest Savings Account (HISA): A low-risk option, assuming an average return of 4.5% p.a. Interest is taxed at the marginal rate.

- S&P/ASX 200 ETF: A diversified investment in Australia's 200 largest companies, assuming a long-term average total return of 8.5% p.a. based on historical performance. Tax is calculated on distributions annually, and capital gains tax (with a 50% discount) is calculated on the growth at the end of the 10-year period.

- Diversified High-Growth ETF (e.g., VDHG): A globally diversified portfolio with a 90% allocation to growth assets, assuming a long-term average total return of 9.5% p.a. based on its long-term strategy and historical data. Tax is calculated in the same manner as the ASX 200 ETF.

The $10,000 Decision – 10-Year Financial Outcome

The following table summarises the net financial position after 10 years for each path. "Net Benefit" compares the outcome of each investment against the benefit of making the HECS repayment (which is the total indexation saved).

$10,000 Decision: 10-Year Financial Outcome

| Decision Path | Initial Action | Final HECS Balance ($) | Final Investment Value (after tax) ($) | Total Indexation Saved ($) | Illustrative 10-Year Outcome ($) vs. Baseline |

|---|---|---|---|---|---|

| Path 1: Repay HECS | Pay $10,000 to ATO | $0 | $0 | $3,588 | $0 (Baseline) |

| Path 2: Invest in HISA | Invest $10,000 in HISA | $0 | $13,757 | $0 | $1,069 |

| Path 2: Invest in ASX 200 ETF | Invest $10,000 in ETF | $0 | $19,005 | $0 | $6,317 |

| Path 2: Invest in High Growth ETF | Invest $10,000 in ETF | $0 | $20,832 | $0 | $8,144 |

Note: These calculations are purely illustrative and based on a specific set of assumptions. HECS balance in all scenarios reaches $0 within the 10-year period due to compulsory repayments. The benefit of Path 1 is the total indexation avoided on the $10,000 portion over the life of that portion of the loan. The Net Benefit of Path 2 is the final after-tax investment value minus the total after-tax value of the HISA (as a proxy for the risk-free rate) and then compared to the indexation saved.

Disclaimer: These calculations do not represent a forecast of actual returns. Your personal financial outcome will vary depending on your individual circumstances, the specific investments chosen, and future market performance.

The analysis clearly demonstrates the power of compounding returns. The guaranteed, tax-free "return" from paying down HECS (equal to the 3.0% indexation rate) is consistently outperformed by the after-tax returns from all investment options over a 10-year horizon. This highlights the significant opportunity cost of using funds to pay down a low-cost, low-risk debt like HECS-HELP for individuals with a long-term investment horizon.

Section 7: How to Decide What's Right for You.

While the numbers often point towards investing, the decision to pay off HECS-HELP debt early is deeply personal and depends on individual goals, risk tolerance, and life stage. The optimal choice is not purely mathematical. This framework is designed to guide an individual through the key considerations to arrive at a decision that is right for them.

A Decision-Making Flowchart

Answering the following questions in order can provide a clear path forward:

- Do you have any high-interest consumer debt (e.g., credit cards, personal loans)?

- YES: Financial principles suggest that paying off high-interest debt is the highest priority before considering other actions, as the interest rates are far higher than any HECS indexation or reliable investment return.

- NO: Proceed to question 2.

- Do you have a fully funded emergency fund (3-6 months of essential living expenses) in a separate savings account?

- NO: A common financial strategy is to build this financial buffer first. It provides security against unexpected events and prevents the need to take on high-interest debt in a crisis.

- YES: Proceed to question 3.

- Are you planning to apply for a mortgage in the next 1-2 years?

- YES: This is a compelling reason to consider early repayment. It's advisable to use a borrowing power calculator or speak to a mortgage broker to determine how your HECS repayments are impacting your maximum loan amount. If paying off your HECS debt is the difference between affording a desired property and not, it may be a strategically sound decision, especially considering the specific policies of lenders like CBA and NAB.

- NO: Proceed to question 4.

- Does the existence of your HECS debt cause you significant psychological stress or anxiety?

- YES: The emotional benefit of being debt-free is a valid factor. If the debt is a constant source of worry, paying it off may be worth the financial opportunity cost for your overall wellbeing.

- NO: Proceed to question 5.

- If you have answered NO to the questions above, do you have a long-term investment horizon (5+ years) and a reasonable tolerance for market fluctuations?

- YES: The mathematical evidence strongly suggests that investing your surplus funds in a diversified portfolio of growth assets, like a low-cost index ETF or into your superannuation, is a financially superior option that will likely lead to greater wealth creation over the long term.

Final Scenarios

To synthesise the framework, consider these final scenarios:

Paying Down Might Be Suitable If:

- You are on the cusp of applying for a home loan, and your HECS repayments are the specific factor preventing you from borrowing the amount you need.

- Your remaining balance is small enough to qualify for a favourable lender policy (e.g., under $20,000 for NAB) that will significantly boost your borrowing power.

- You are highly debt-averse, and the psychological benefit of being debt-free outweighs the potential investment gains.

- You have already maximised your tax-advantaged investment options (like superannuation) and have no other financial goals that require liquidity.

Investing Could Be a Stronger Option If:

- You have cleared all high-interest consumer debt and have a secure emergency fund.

- Your primary goal is long-term wealth creation.

- You are saving for a home deposit, where every dollar of capital is critical.

- You value financial flexibility and liquidity, recognising that voluntary HECS repayments are non-refundable.

Conclusion: Your HECS, Your Strategy

So, after all that, what’s the final verdict on HECS? The national conversation around HECS-HELP debt has undergone a dramatic transformation. The indexation shock of 2023 forced a re-evaluation of a loan that many had comfortably ignored for years. In response, the Australian government has implemented a suite of reforms—capping indexation, cutting principal balances, and easing repayment burdens—that have fundamentally de-risked the scheme for the long term.

The analysis indicates that for most individuals with a long-term perspective, the mathematical case is clear: the opportunity cost of paying down HECS-HELP debt early is significant. The potential returns from investing in diversified growth assets or the guaranteed, tax-free return from a mortgage offset account are highly likely to outperform the capped HECS indexation rate over time.

However, the single, critical exception remains its impact on mortgage serviceability. For aspiring homeowners, HECS-HELP debt can be a direct and substantial barrier, reducing borrowing capacity at a crucial life stage. The emerging, more nuanced policies from major lenders create specific situations where a strategic, targeted repayment can be the key that unlocks home ownership.

Ultimately, there is no single right answer. The decision rests on a careful evaluation of one's personal financial situation, life goals, and risk tolerance. By understanding the mechanics of the system, the implications of recent reforms, and the trade-offs involved, every Australian with a HECS-HELP debt is now better equipped to make a confident and informed choice that aligns with their unique financial journey.

Enjoyed this breakdown?

For more detailed guides and visual explanations on Australian finance, make sure to subscribe to the Wealth Copilot YouTube channel.

Subscribe on YouTube